Impending system collapse?

Is this inflation the beginning of the end of the dollar? It depends

Trialling the new audio feature below, if you are on the go! I add a fair bit of discussion, theory, context and history to the piece.

I wrote a few articles earlier in the year, and looking back, it seems I was at least focusing on the right topics. I got a few things wrong, but given the staggering speed at which events are occurring, most people’s predictions are also a little off, especially those in power. Remember when the war in Ukraine started, Russia was going to go broke due to Western sanctions? Here’s economist Steven Hamilton of George Washington University predicting the effects of the massive Western sanctions and seizures of foreign currency reserves:

“This is going to generate a kind of currency crisis, financial crisis, and an economic crisis in Russia, and the sanctions make it very difficult for the Bank of Russia to do a lot of things that it would normally do to try and control that situation.”

So, one takes a quick glance at the Rouble and expect it to be toast?

Not quite. The reasons for this are many, but safe to say, when a whole continent decides it cannot purchase its electricity from a cheap & reliable pipelined source, a global run will occur on those now scarce resources, and the country with said resources can ride that wave of supply side inflation all the way to the bank. Russia’s current account surplus has tripled since the beginning of the war. Needless to say, all this money coming into the Kremlin makes it quite easy for Russia to continue the war through the winter.

So, if our economists informing our foreign policy decisions are getting it so so wrong, do they at least have some control of the situation at home? How about other facets of the economic war? Surely there are policies in place to deal with the sanction-enforced energy crisis?

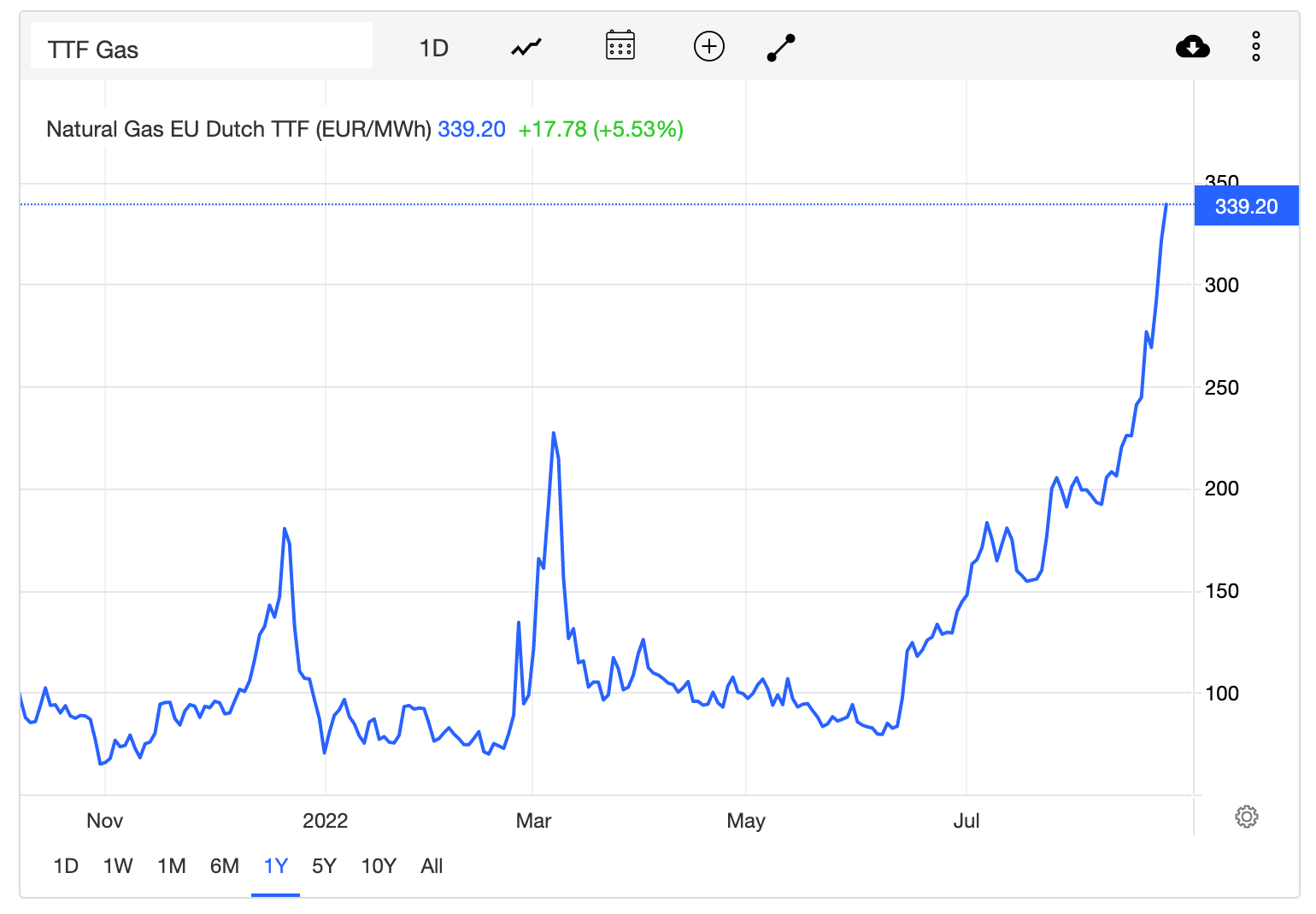

A tripling in the price of EU gas prices would point to say no. Short of nationalising the energy companies or banning futures trading on commodities, there isn’t much anyone can or will do to bring this down. These policy options exist because they once existed, and do work. But politicians are bought and paid for by the fossil fuel companies, so it is the people who must pay. The world runs on energy, and currently that means using fossil fuels. There is no easy, quick, painless solution in moving to renewables, especially not when China produces 75% of all renewable tech and infrastructure.

It cannot be emphasised enough how important the energy crisis is. The fate of the Western alliance and in turn the US dollar rests on Europe making it through the winter(s). In turn, the rest of the world watches, hedging its bets. Everyday Europeans and businesses are being asked to undertake a massive sacrifice, one upon which history will either view as a noble act of devotion to US liberalism, or a fatal self-inflicted wound.

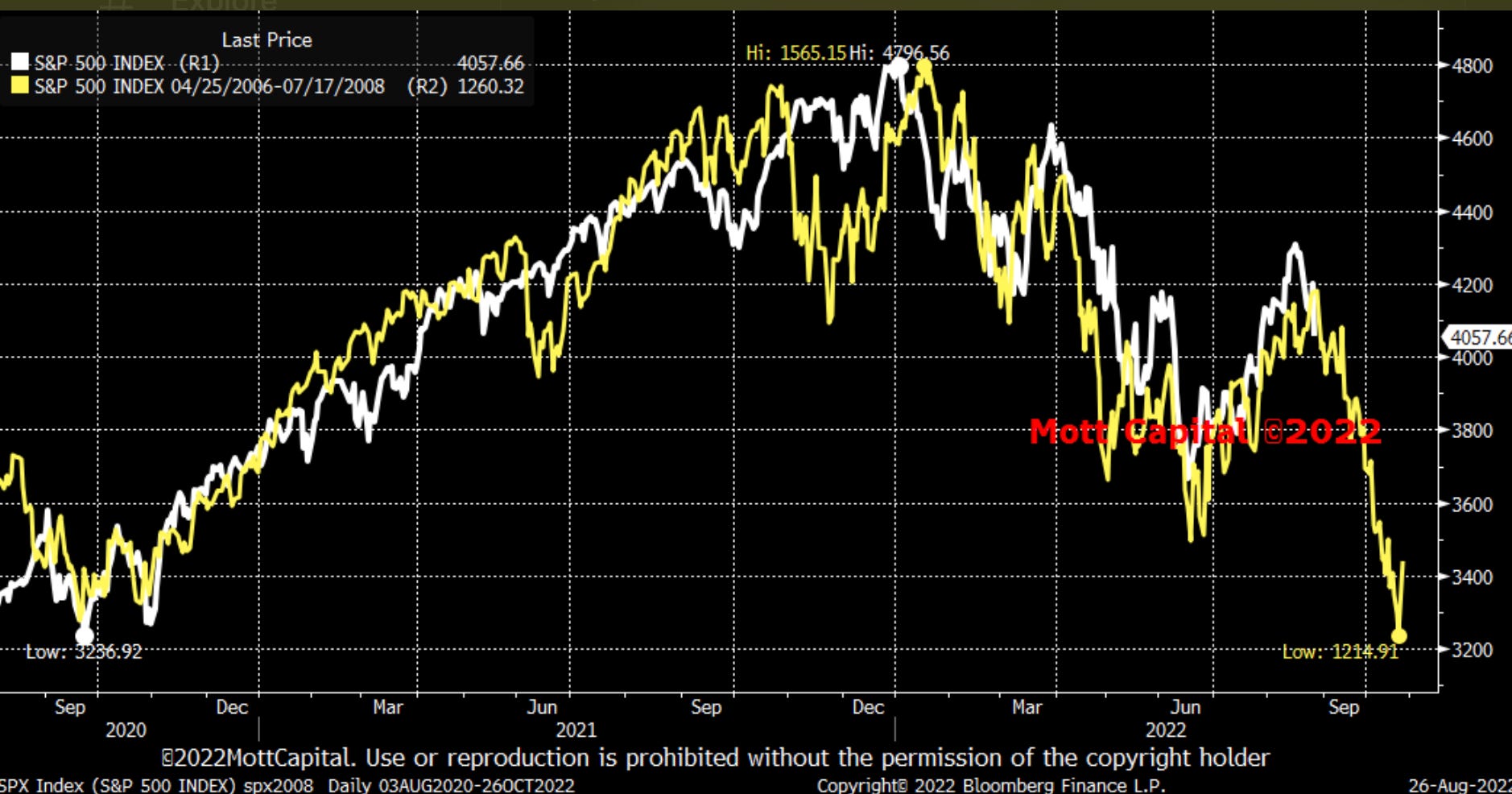

Over in the US, the markets are performing an almost synchronised replication of the 2008 crash, indicating there is something massive on the horizon. Check this out (history doesn’t repeat, it rhymes etc)

Central Banks across the world continue to tighten financial conditions in an attempt to control inflation. Chairman Powell was adamant yesterday at Jackson Hole that the Fed will pursue price stability, no matter what the markets say. It seems everyone knows that a crisis is unfolding, and that it just is a matter of how big the crash is, and what policies will be used to treat the symptoms. This newsletter is a signpost in time: what could occur? Is this the end of the dollar? Will the geopolitical risks materialise and destroy the whole system?

Firstly, a few bits I’ve pointed out in earlier newsletters:

China saved the world in the aftermath of the GFC through its massive stimulus binge on property and infrastructure.

It can’t and won’t be happening again, as Xi has decided to get ahead of the curve and try to control the collapse of the Chinese real estate bubble

There is no slack left in the system for the Fed to cut rates to deal with the impending crash, and even if they wanted to, you’d still have inflation running way above target

The US, across the globe, is risking catastrophe in an attempt to maintain its dominant position. The logic of empire demands this. Everything must be seen as a high-stakes gamble with real risks, because no longer can the US act with impunity. Real challengers, with nuclear weapons, are pushing back.

Values are immaterial to the overall goal of maintaining US hegemony: keeping Saudi Arabia onside matters more than anything else. No idea of human rights or universal liberal values can be considered, due to the above realities

With all this in mind, let’s consider some possibilities that could occur in the coming months. Firstly, with the passing of the Inflation Reduction Act (IRA), and the CHIPS semiconductor re-shoring program, it seems the American elite has somewhat settled its domestic policy settings for the upcoming Cold War 2. Energy wise, the US has hedged its bets, approving massive amounts of fossil fuel exploration and licensing, but also agreeing to a decent sized investment in renewables. As stated above, China has cornered the market on renewables up to now, and the US knows that it needs to at least be able to point to a growing domestic industry to be taken seriously as a ‘global leader’ on climate change. It also gives the fossil fuel companies a nice handout of R&D cash. Safe to say though, if the Republicans get in 2024, this nascent renewable industry will be the first to go. Suits everyone then.

The CHIPS act is far more consequential. The US is finally waking to the reality that in a moment of crisis, it will be unlikely to be able to defend its semiconductor factories (Taiwan and South Korea) in the event of a conflict. It must develop its own semiconductor industry ASAP in order to maintain the missile and weapon supplies it depends on for its military dominance. The US has significantly diminished its stocks of high-tech weaponry in supplying Ukraine, which may be good for the revenues of the military industrial complex in the short term, but long term presents some massive challenges. The US aims to turn Taiwan into a ‘porcupine’, a little island of spikes, also known as missile, that China cannot reclaim as its territory. The US is in a race to develop its technological industries, against China’s willingness to act on Taiwan. I must point out, the ‘porcupine’ tactic failed in Ukraine. Indeed, it was one of the main reasons why Putin invaded: to act early and stop the ‘spikes’ being assembled on his border. This is called the security dilemma in international relations, and it’s an unfortunate reality of statecraft. One man’s idea of defence is viewed as an offensive measure by everyone else.

This is the unfortunate feeling I get about the current moment, particularly after totally seeing and calling the Russian invasion wrong. The best case scenario is China continues its rise, comfortable in the belief of the eventual demise of the US, and assured of its final ascension to global primacy. In this instance, Taiwan will return to the fold of One China peacefully in time. More likely though, China sees the United States in a state of disarray and chaos, and understands if it acts now or soon to take Taiwan, it can take the opportunity to prevent a nasty ‘porcupine’ on its border. It will also cripple American prestige, the collective belief of unassailable US dominance that results from a network of 750 military bases around the globe. At that point, anything is possible.

Back to the economic crisis. Leaving aside what China may or may not do, which is unknown, we turn to Saudi Arabia, which holds the key to the US fate. Much was made of Biden’s recent trip to Riyadh, apparently to ask for more oil to help lower the price at the pump back home, easing inflation in time for the upcoming midterm elections in November. And this may be true, although given that MBS (everyone’s favourite moderate) has been meeting Putin every other month, its more likely bigger, far more consequential issues were on the table for discussion.

Specifically, one of the main objectives of Biden’s trip would be to shore Saudi support for the US dollar. One of the fairly foreseeable consequences of the sanctions on Russian participation in many international financial systems would be proposals to create their own networks to settle payments. Indeed, China has been attempting to push the digital renminbi as such an option for a few years, arguing the massive amount of trade of Chinese-made physical goods rivals the US petrodollar for importance as status of a global reserve. Most countries in the ‘global south’ were receptive to the idea, and in the face of the upcoming conflict, even more so. India, Brazil and Iran are key to watch in the coming years. But in the short term, all rests on Saudi Arabia. Aramco (Arab American Company), the oil company owned by the Saudi family, has always asked for US dollars for its crude, but this may be about to change. As the global chess board flips, many middle countries, central to the global economy and currency stability, are keenly observing the current unfolding crisis. If the Saudis flip, and join the developing rouble/renminbi exchange bloc, the dollar may be terminally damaged. At that point, who knows what may happen.

Back to Europe, and even more concerning and immediate, the unfolding energy crisis will blow up the European markets. The Italian bond market is months, maybe weeks away from total collapse. The sky high energy prices are causing mass de-industrialisation events across the continent, which are being cheered by the green movement as the first steps in a ‘transition’ to a ‘green’ economy. Personally, I am skeptical.

In the face of decades of failure to significantly legislate de-carbonisation of the economy, it seems European politicians have internalised their powerlessness to challenge special interests (probably because they eat at the same table). Unable to counter the needs of the fossil fuel companies or Norway, and the cravings of German industry for cheap Russian gas, European elites have grabbed the chance to blame Putin for the war as the cause for the energy and economic crisis. The reality is this: the fossil fuel companies are absolutely raking it in right now, and mentioned earlier, so is Saudi Arabia. The US, as a net energy exporter, also benefits from the price spikes. But it also gives the ‘green’ movement, mostly enabled by the centre-left coalition in Germany and the World Economic Forum Davos set, a chance to implement its desired policies of ‘de-industrialisation’ for the first real time at scale. It’s critical to understand the general European sensibility on the green issue: it is as valuable to them and their identity as US primacy is to Americans. In many ways, the war provides cover to pursue policy goals that otherwise the general populace might have well founded objections to.

As stated earlier, everyday Europeans are now tasked with a winter of rationed energy, massive job losses, cold showers and the rest. That’s why I am sceptical of the ‘transition’: everyday people are being handed a monumental burden, without any real support, warning or assistance. To expect there not to be protests, massive civil unrest and the potential for a resurgent far-right reaction is stupid hubris from the elites pursuing these policies. People will react, and we should expect violence. All the while, there will be calls to end the war in Ukraine, which builds the narrative of a choice between what Macron calls “abundance” and the lives of Ukrainians. The fact is, a lot of people see that war as unnecessary. More importantly, they see their own suffering to be futile too. If the protests gather momentum, who knows what occurs. The potential for a rerun of 1930s-style European fascism is not small, and at that point, just as the German aristocracy, Henry Ford, some of the British royals and many others initially welcomed Hitler to counter the threat from the East, so too will European industrial and banking wealth desire a movement and authoritarian to placate the masses. Unfortunately, at that stage, the ‘green’ dream will appear the chimera it likely is.

Currently, European policy makers are arguing there is an existential threat to liberty in the East, whilst simultaneously defending the impending energy-induced economic collapse as a necessary condition to fight climate change. I am not sure how the second policy goal assists the first, but at this stage, who knows what is really going on behind closed doors. The whole while, the US continues to send weapons and troops to Europe. Given the likelihood of massive political unrest as events unfold, everything depends on what has been termed ‘European solidarity’ in continuing to support the war in Ukraine. In this respect, NATO pledging to increase its standing high-alert force sevenfold to 300,000 troops seems quite an effective insurance policy against both the Russians and internal European dissent.

It’s not that these eventualities are certain: it’s that escalation becomes far more likely the further down the road we go. The US has decided it will not go quietly. I think this is a fairly uncontroversial statement at this point in world history, especially when one considers all the actions it deemed necessary along the way to now: Hiroshima & Nagasaki, Korea, Vietnam, Afghanistan and Iraq, and all the other secret coups and civil wars: the evidence is irrefutable. So no matter what else occurs, it is probably wise to view all American government actions, as we do Chinese or Russian, as in the interest of the pursuit of power, militarily, culturally and economic.

So in conclusion, what does all this mean for the dollar? What about inflation? Well, here’s my thesis for the next little bit.

Firstly, the Fed will continue to raise rates until it breaks something. The recent bull rally in the share market imploded overnight after Powell’s speech, and as shown above, there is a lot of room to go down. The ‘wealth effect’, the euphemistic terminology for what you believe your house is worth, is about to get hammered. Combined with the energy crisis, a rather massive global recession is already baked in the cake. But inflation will remain. The hope that it will disappear is naive at best.

All the geopolitical factors point to a higher inflationary environment. Biden approved the highest ever military budget this year. The CHIPS act is a massive stimulus. The IRA, far from reducing inflation, is another stimulus. The administration claims the bill will create 60,000 high paying ‘green’ manufacturing jobs. Not a week goes by without another couple hundred million in for weaponry to Ukraine, not to mention the promise of rebuilding the destroyed country. As Europe continues to build its armed forces, orders for the US military contractors will continue to come in. All these factors mean more dollars need to be printed, and are highly inflationary for the domestic US economy, and will be for some time. As much as the Fed tries to convince markets it will control inflation, the US government will row the other way with its massive deficit spending.

Globally, as rates rise, high debt nations will be crippled by higher rates and depreciating currencies (see Sri Lanka). More and more of these smaller nations will turn to other methods for financing and for settling payments, and other patronages for defence and support. The great de-globalisation about to occur will likely reduce the role of the US dollar in favour of the rouble/renminbi. However, given the outstanding debt the US owes as well, the US must maintain dollar hegemony. It cannot allow the dollar to implode, as it would mean financial ruin. This is a very real risk in the medium term for the US, and would likely precipitate or coincide with total war, as has all other historical instances of currency collapse of this scale.

So the Federal Reserve, the Treasury, and the US military all must compromise to certain degrees. There is no easy solution, no option that settles all policy goals without massive blowback from a variety of sources. Raising rates to 10% will bankrupt the government. To maintain the US dollars primary role in international affairs, to keep people believing the dollar is worth something, the US government must undertake a massive increase in debt and deficit spending on the military and technology. The bond market may blow up, but it too may be sacrificed as an emergency measure in war. Nowhere is safe if this occurs.

Inflation will continue to bubble away in this environment. Handily, inflation continuing at an elevated level will assist in reducing the relative size of the massive US government deficit. Wages will likely continue to go backwards in real terms, but this also will temper demand, helpful for the green cause. The people may suffer, just as in Europe, but the powerful, not so much. And in the end, that’s the main goal.

Anyway if you got this far thanks for reading, I appreciate it, and any insights or commentary you’d like to add, let me know!