Money, heaps of it

Central banks have lost control. Wish us luck

Another week in isolation for myself gives me ample opportunity to write. Continuing on from last week’s discussion of government debt, this newsletter will focus on the overall money supply. It’s quite a complicated issue; with the help of a few graphs, we should be able to dig down a bit further into what is occurring in the global economy. The consequences of central bank policy will be the story of the next few years, and it pays to have some understanding of the chi of our economic system.

Last newsletter was an attempt to counter the myth of the ever growing free market. Government spending, particularly decisions to engage in stimulus funded by budgetary deficit, have been the main driver of growth and markets for the past 20 years. Often times, these decisions to raid the public purse are the political response to central banks and private banks catastrophically over-stretching their lending, tanking the whole economy. For reference, Matt Taibbi’s excellent Griftopia covers most all of the shocking double-dealing and market manipulation on Wall St in the lead up to the GFC. Films like the Big Short manage to conjure a hero out of the crisis; the truth is a story featuring villains of unimaginable greed and viciousness, escaping consequence and in most cases benefitting from government bail outs.

We will leave bailouts for the moment, and their political implications, and start with the hottest topic in finance, the largest experimental economic program ever undertaken, ‘quantitative easing’. This is one of the biggest stories of the pandemic, on par to the obvious health implications of the pandemic. It should be on the front page as often as the epidemiological analysis of what is occurring, and deserves far more coverage than any tennis player or Prince (Harry, that is. The Andrew formerly known as Prince has a whole lot to answer for). Central banks play an outsize role in everyday life, but their work is mystified to the point of mass confusion. Let’s break it down.

In early 2020, markets crashed worldwide in response to the massive collapse of production and consumption engendered by the first wave of the pandemic. Central banks, the wizards of global finance, were faced with a severe crisis. Governments seemed committed to massive deficit spending. However, in the short-term, financial markets began to seize. When the money stops flowing, the whole system is at risk. In response, central bankers decided to go spray the markets with money. Lots of it. Shown here is M3, total money in the United States, consisting of notes and coin, deposits, funds etc:

This is not controlled by the government: the US Federal Reserve (the Fed) is a private conglomeration of bankers that decides on the conditions upon which commercial banks can borrow funds (the cash rate, which feeds into bank interest rates, is how most regular people interact with the Fed). The Fed flooded the market with almost free money to banks and financial funds, who in turn can lend it on to consumers or corporations at a profit. The Fed’s role in normal times is to “take the punchbowl away before the party gets rowdy”, i.e. not let interest rates be so low that risky lending takes over. Faced with the crisis of the pandemic, the Fed decided to spike the punchbowl with any leftover liquor lying around. Here’s their balance sheet, i.e. total assets purchased by the Fed through the creation of ‘money’. Look at that rise!

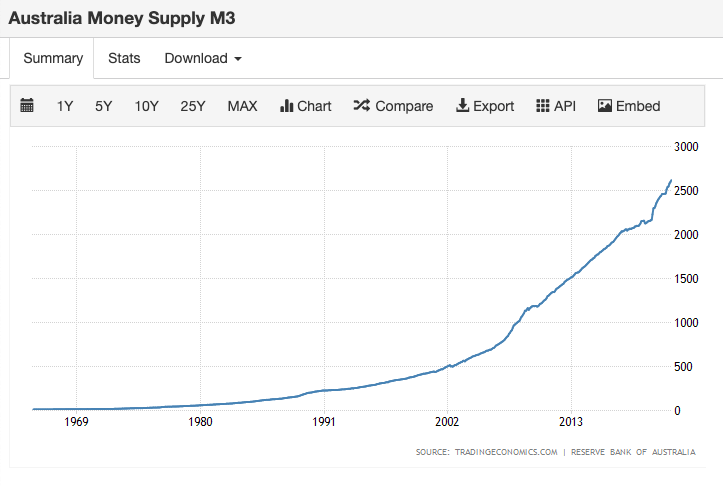

These values are almost impossible to comprehend, but for reference, overall money supply has increased almost $6 trillion in 2 years. That’s more money thrown into circulation over 24 months than the 30 year period from 1970 to 2000. The Fed has done this through a combination of dropping interest rates to emergency record lows, and the purchase of government bonds and other financial assets in order to inject money in the system. This program, quantitative easing, was first trialled in Japan by their central bank in response to its cratering economy in the 90s. It was used by the Fed and the European Central Bank in response to the GFC (2007-2008 in the graph above). And whilst we in Australia only officially joined the party in 2020, our long term trajectory is broadly reflective of overseas trends:

Now, all this extra money has to go somewhere. Those already with assets to be used as collateral will take it on as debt, and invest it. The whole idea of the program is to stimulate business lending, but guess where it actually goes: asset values (houses, classic cars, commercial real estate), equity values (shares and stocks), new speculative tokens (cryptocurrencies). When you overlay the parabolic upward trend in overall money supply next to these financial ‘markets’, we see something quite remarkable. Here’s the S&P500 index, a measure of large US companies stock values, as compared to overall money supply.

Or everyone’s new favourite investment vehicle, cryptocurrency. Here’s the total market capitalisation, determined by a simple ‘token x value’ calculation.

Having seen the previous graphs, it doesn’t take much imagination to wonder how digital tokens with no dividend, no rent, and no productive capacity in the traditional sense, have increased in ‘value’ to be worth as much as major industries, such as the global oil and gas drilling sector (roughly $2 trillion). Forget the morality of burning fossil fuels for a second, and just think of how much of all we see and do is powered or produced with hydrocarbons, whether it be transport, plastics, electricity, or any of the other myriad uses we rely upon in everyday modern life. And then think of DogeCoin. Something is seriously amiss. Even a supposed useful token such as Ether has a greater market capitalisation than the GDP of Norway, a wealthy developed country of 6 million people. The notion of value in our economy is collapsing, and Crypto is the canary in the coal mine.

Another example is Tesla. Worth more than the nine largest carmakers around the globe combined, Tesla produces less than 1% of global car sales. This is mass hysteria, enabled by the easy monetary conditions of the Fed. In reference to the punchbowl at the party, at this stage its looks like quaaludes and LSD have been added to the mix, rather than our grandparents whisky or brandy. A party like this will inevitably lead to a mighty hangover.

So, as we can see, it is systemic movements in the background of the economic system that are determining the perception of value. Just as we saw how government debt is sustaining national economies, we can also see that central banks are juicing the system to an extreme degree. There should be no mystery as to why they are doing this: the ongoing insider trading scandal at the Fed is proof enough to understand whose interest they serve. But it is crucial to understanding why we are undergoing a ‘boom’ in the middle of a pandemic, with all the ensuing supply chain issues, job losses, suppressed demand, and inability to travel and gather freely. There is no boom, as we would like to think there is. There is a massive pile of fake money being thrown into the system making people feel wealthy. A whole range of consequences are starting to develop in the system, from minor to potentially catastrophic. The currency is beginning to lose its worth, and the resultant inflation scare is where the real danger lies.

It is quite simple: inflation is taking hold, and there are only two options to control inflation. The current bout of inflation is very conditional on the pandemic and supply chains, but either way, the perception of future price rises engenders current price gouging. The options are either to increase taxes to slow spending, or increase interest rates to slow spending. No political party has the appetite for increasing taxes, hence the responsibility for slowing inflation falls to central bankers. When rates increase, not only do consumers pay more on their mortgage, banks and corporations also have to pay higher servicing costs on commercial loans. Further, government debt becomes more expensive to manage. This leads to a contraction of overall lending and spending in the system, as fund managers and governments look to cover higher interest payments. This can have a domino effect in the system, or people call in debts simultaneously, leading to a credit crunch and defaults. These are all possibilities on the economic horizon for the next few years.

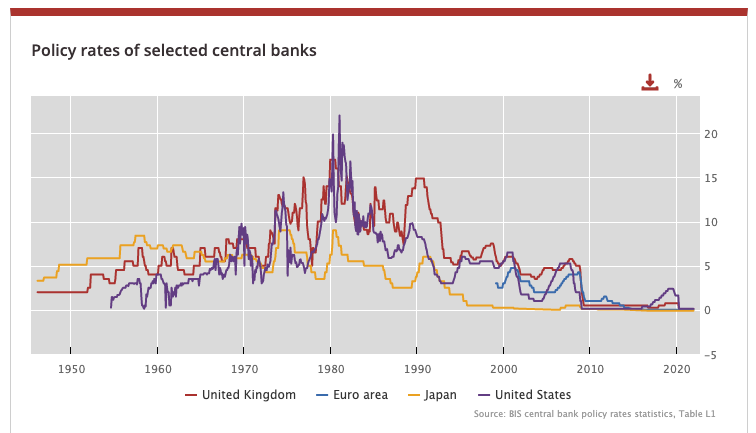

It is critically important to note that the global trend towards central bank quantitative easing has followed a strong trajectory of loosening interest rates. This has been for a variety of reasons, but mostly by attempts of central banks to stimulate their respective economies as growth rates have decreased.

When combined with government deficit spending discussed last week, we can see that policy makers have been rather desperately trying to create growth over the past 30 years. Over time though, it doesn’t appear to be working. Quantitative easing is the last resort for central banks when they can’t cut rates any further. Faced with a crisis, and if rates are already low, the only option is to turn on the digital printing press. As we can see, Japan used their ammunition in the 90s, and have been buying bonds and financial assets since to sustain their economy. Japans growth has never fully returned, despite the emergency measures.

The deeper question is where has it all gone wrong? Why is there no growth outside of debt and deficit? What has happened to the major capitalist economies? The answer is globalisation, but that’s a topic for another newsletter. The main point of this paper is to illustrate how drastic current policy settings are. Free money for the rich is distorting every commodity and equity market across the globe. In a world where debt is everywhere but also simultaneously the driver of growth and value, what happens when interest rates inevitably increase? Overall global debt has risen from $250 trillion in 2018 to $300 trillion at the end of last year. All that debt, even though it’s highly unlikely to be paid back in full, requires interest payments in the short term.

How do we counter inflation, if in doing so, it could cause the ultimate of all bubbles to burst? Governments will be forced to turn to debt and deficit spending again, or face total collapse in consumer spending and confidence. Combined with the need for drastic investment in new technologies to drive renewable energy, policy makers are facing a fast approaching inflation iceberg. We will bear the consequences of 30 years of loose monetary policy in the coming years.

In the next newsletter, I plan to take on the “banking cartel” head on. But to do so, one has to have a broad overview of the global conditions upon which the current situation has developed. Hopefully this newsletter has provided a glimpse into how much “value” has been created in the economy by the policy decisions of central banks. People regard themselves as wise investors when conditions allow such flattery, but I do wonder how that will change as these forces manifest. In the recent past, we have all had time to ourselves to reconsider what value looks like. It may need further revision over the coming years.