2022... Meet the new boss, same as the old boss

Deficits are nothing new. What we do with them matters.

Happy new year. Despite the current doomsday mood sweeping the nation, 2022 promises to be the year we find a path forward through the pandemic. Let’s hope so. But rather than write an article on the misdirection of the media and politicians regarding Novaxx Djokovic, or another rather pointless epidemiological analysis (who trusts the data at this point?), let’s return to the usual fare: economics, finance, debt. Covid-19 will pass, in time. Banking and state power is rather more stubborn. Meet the new boss, same as the old boss.

Regard this article as an addendum to the previous newsletter, which explored Dylan Alcott’s political aspirations, in light of his allegiances to ANZ, Uber, and Nike. Feedback to the article was both positive and negative, but what I found most curious was the apathy. Many people I’ve spoken to wonder why I am so sharply critical of these corporations, why I refer to an “Australian Banking Cartel”, and so on. In light of the massive rise in house prices, shares, and digital tokens, many on the high side of this exchange respond indignantly to suggestions that anything other than outcomes of a “free market” are occurring. In this post (and this is probably the central thesis of this newsletter and project), I will try my best to dispel the mythos of free market capitalism, particularly in its Australian context. When we have a Prime Minister ranting that “can-do capitalism” can solve climate change, we are well down a rabbit hole of delusion and deceit that needs fumigating. But do that, we need to take a deeper look at some of the fundamentals of the “free market”.

Let’s take a look at the United States, the strongest capitalist economy in the world. We are taught that the US defeated the Soviet Union and communism due to the superior power of capitalism and its ability to distribute resources and produce goods. This is one of those truths we hold self-evident (if you’ll indulge me). Further, we are taught that it is only the free market, and not government spending, that can grow an economy. This is liberal economic theory 101. Everyone knows this: a government can’t spend more than it taxes, lest it fall into deficit. The government should not intervene in the free running of the private market, as it is the private free market which enables all the good things we take for granted, from TVs to smartphones to cars. Money in the private economy is always invested far wiser than capital doled out by centralised fiat. Government should be limited in scope and size to enable this, which in turn means government spending shouldn’t be required for the engine of capitalism to deliver growth and prosperity. This is accepted economic theory of both major political parties in the United States, Britain, the Euro and Australia, and by the technocratic bureaucracy that runs our economic systems.

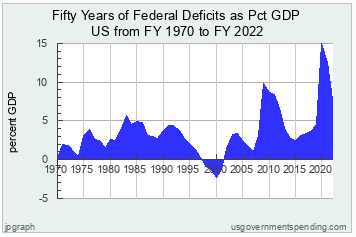

What you’re seeing here is how much more money the US government is spending compared to its revenue, year on year, over the past 50 years, as a ratio to overall economic production (GDP). As we can see, it was only for a small period between 1997 and 2003 that revenue exceeded spending. At all other points, the government was massively spending above a balanced level to prop up the economy. But it’s not as if all this government spending has resulted in massive levels of growth:

Quite the contrary: what these graphs show is that without massive levels of government spending, the US economy would be going backwards at an average rate of roughly 4-5% every year. The American private “free market”, whatever that is, the supposed engine of global capitalism, can’t sustain itself, and has been shrinking in size since at least 2000. It is only massive deficit spending by the government that maintains the economy of the United States. It is not the ingenuity of the free market, Adam Smith’s invisible hand, or the “destructive/creative” power of capitalism at work. It is government debt that is doing the work.

Now, this might not seem of all that much consequence to you. But it is the essential historical insight of the 20th century mentioned earlier reframed: it was not the free market capitalist model of the United States that won the Cold War; rather, it was the ability of the US government to borrow and spend money far above its revenue that has been the prime driver of its economic system over the past 50 years. Without it, the economy collapses.

All those deficits from the past add up to a total current US government debt of nearly 30 trillion US dollars. That’s nearly $90,000 owed per citizen. It increases at a rate of $100,000 every 4 seconds. Everybody knows that it cannot possibly be repaid.

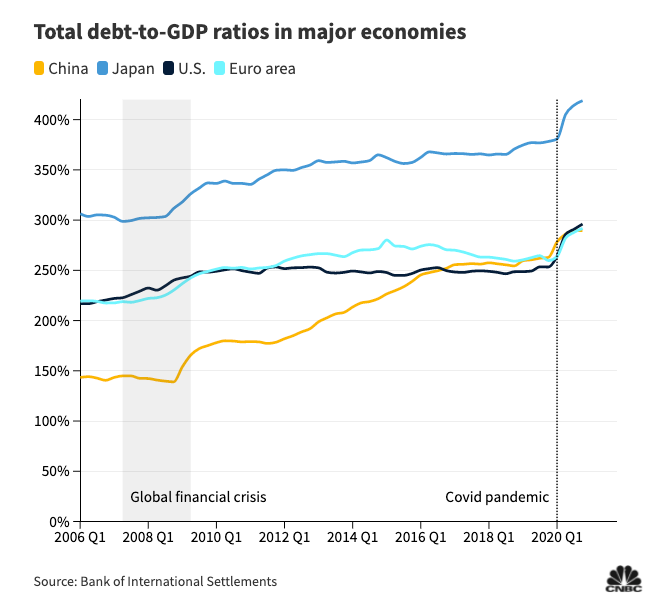

It’s also important to note that it isn’t just the Americans who rely on this model of deficit spending to maintain growth. Most of the “major advanced economies” as they are known, are swimming in debt way above the OECD average (black dots below).

Those who hear my politics know I’m not necessarily advocating for less government spending (although I used to): it’s always been a question of what the money is being spent on. The central insight is the basic characterisation of the economy as a free market of trade and finance is a myth. It isn’t simply about the exchanges of goods, profit and loss, and balancing budgets; because if it were, why would there need to be such a universal trend of un-payable debt to sustain the system? We, as atoms in the system at the micro level, have to see and act in the old fashioned way: we must repay our debts. However, at the global macro level, the actual level of consequence and importance, politics and state power are the forces at work, rather than the myth of the market. It’s no secret that these debts will not be paid.

You may ask, what does this have to do with Australia? What does this have to do with our banks? What does it matter? Well, firstly, our federal government is approaching the 100% debt-GDP ratio. We are well underway a new economic/governance paradigm, where the Liberals previous freak-outs about debt have been quietly forgotten (remember Rudd’s GFC spending?). Debt is ballooning all around. If government spending is required to sustain the economy, we should think long and hard about where we direct it for the next 50 years. Renewable energy rather than fossil-fuel subsidies, public transport rather than Electric Vehicle (EV) infrastructure (yes), local manufacturing rather than strip-mining the whole joint and sending resources overseas. These are essentials. The Liberals will rant and rave about debt if they lose the next election, they might even be shameless enough to talk about it in the campaign, but both parties know the debt can’t be repaid. It is simply a question of where we direct spending from here. There is no sustaining free-market without government spending and regulation. Basic insight, but easily mistaken by most.

And one final point: the major economic factor of our fortune for the past two decades, demand for the natural resources of this continent, can no longer be guaranteed to save the day. This is not fear-mongering, because we may get by on the EV revolution and its insatiable appetite for lithium and other rare earth minerals. However, in regards to our largest export, iron ore, times are changing, and we best understand what is happening. Neatly, it links back to government deficit and debt. In this case, Chinese state debt:

The global financial crisis provided a rude shock to the Chinese economy. As global employment and income dropped, and demand for goods and services sank, China as the worlds manufacturer faced a conundrum. Without exports, it needed to stimulate its own economy desperately, or face a crippling recession. In response, the CCP implemented a massive infrastructure and construction stimulus program, one of the largest injections of debt into an economy ever. It did this through both government deficit spending and lending by state-owned banks. Funding flowed for highways, skyscrapers, public transport, which all require high-grade iron ore for steel. More concrete was poured in 3 years than the whole 20th century in the US. We were happy to contribute: in the 2007-2008 financial year, around 13 per cent of Australia’s exports were bound for the Middle Kingdom. By 2020, it was roughly half.

Thankfully we are buying US submarines and tanks to scare China. What else can we do?

The income generated from these exports, that we in the cities of Australia can barely comprehend, is what has sustained us for the past 20 years. All this focus on tech and start-ups like Afterpay miss the forest for the trees. In simple terms, it was the Chinese governments decision to undertake massive deficit and stimulus that saved our economy (Rudd’s stimulus helped, but let’s be real). Lucky the agreed term for the period was the Global Financial Crisis, because it truly was an issue that happened elsewhere.

Globally, the catastrophic economic hit to the working and middle class led to severe political consequence: the election of Trump and Brexit, nationalist resurgence on continental Europe. It is pretty easy to imagine the Australia of today, with all its social fracture and class divisions, even angrier, if the economy hadn’t totally rolled over. Most of the youth of the developed world have faced socially downwardly mobile conditions for the past decade. We avoided that fate due to fortune, and we best identify that fortune, because self-congratulation is both unedifying and useless. Scomo’s incantation of “can-do capitalism” to fix climate change is possibly the most dangerous example of this delusion. It won’t cut it. We cannot rely on China to stimulate their economy forever, so we better diversify our economy quick smart. This requires vision and direction from the one sovereign with the ability to do so: the government.

If you remember, a couple newsletters ago I spoke about Evergrande, the Chinese real estate developer in deep debt. The house of cards is slowly collapsing through cascading defaults, and Xi and the CCP seem intent on following through with the controlled demolition of their debt. If the Chinese real estate sector collapses, no apartment buildings requiring high quality iron ore will be built for a long while. This is a risk that is realising in slow-motion. If it were to be combined with a global debt contagion, given the absurd levels of debt in the system outlined earlier, we are mighty exposed. Interesting times indeed, and who in their right mind looks at any of our politicians as having the vision and courage to propose a plan to work through these issues.

Next issue I will hopefully tackle the big one: central banks, interest rates, and banking cartels. Housing prices are a symptom of a wider corruption, one which requires deep discussion. Thanks for reading, and hope all are doing well.