Evergrande - NeverLand

The Chinese now plan to demolish the world economy, one real estate bubble at a time

After last month's newsletter, which quite presciently highlighted anti-Chinese sentiment in the national media, yours truly has decided to continue down this particular avenue of inquiry for a short while. Not to sing the praise of Xi, or the Chinese Communist Party, or indeed any government. We need to be clear eyed in our assessments of the world upon which we gaze; I imagine most of us at this point live in a constant battle between fantasizing for a return to normalcy, and a deeper knowing that normal isn’t returning, because it was never there to begin with.

The normal that we thought we knew, American global hegemony in politics, economics, finance and culture, is being severely challenged by a multitude of factors. China is but one of them. The absolute focus of critique and anger is going to be directed at the Chinese Dragon, in a whole range of ways. Stories of Chinese military aggression, diplomatic coercion, trade deception, and technological theft already fill column after column; this newsletter will only seek to inject some historical couplets to the conversation. History doesn’t repeat itself, it rhymes.

The Chinese are indeed stepping up to the role of Player 2 on the global geopolitical chessboard, but it would be naive to assume they are implementing novel untried strategies. Most Chinese soft power actions have been studiously cribbed from the US playbook of the 20th century. Let’s take a look, specifically in relation to the current crisis facing China and the global economy: the cascading default of Chinese property development group, Evergrande, and its potential to be the first domino to fall in a global debt contagion.

Firstly, as a matter of procedure, the usual caveats. Chinese repression of the Tibetan people, of the Uighurs in Xinjiang, of LGBT minorities, of freedom of thought and expression, and overall labor rights, is abhorrent. As is the criminal justice system in the US (highest incarceration rate in the world), abortion laws in Texas, global drone warfare undertaken by pilots in Virginia, CIA meddling in foreign governments, and the wholesale destruction of local voting rights. The point is not to engage in ‘whataboutism’, the aim is to avoid such comparisons. They merely serve either interest, rather than illuminating any truth about the situation. We would do well, as a country, to attempt this. Instead, we have just signed up to the US nuclear club, in order to combat China, our major trading partner! The next period of Australian history is going to be us attempting to walk the tightrope between these contradictions: who has any hope our politicians are up to the task. The next 5 years will be punctuated by flashpoints of bluster, frustration and finger-wagging, rather than outright conflict. Combined with an eventual charge of responsibility for the pandemic, Chinese intransigence and belligerence will be the story of the 2020s. Here comes another developing story in Western media: Xi is undertaking a controlled demolition of the Chinese market economy, and in turn the global economy, for his own ends.

The Evergrande saga is the catalyst for this explosion. One can find detailed analysis of Evergrande and the wider Chinese realty bubble all over the web; for this newsletter, all you need to know is Evergrande is the world's most indebted company, owing more than $300 billion (USD). It amassed this debt raising funds to build apartments in the rapidly urbanising Chinese market, which is now comfortably the largest real-estate bubble in history. For decades, Evergrande would borrow money from anyone who would lend it; cheap money from across the globe flew in due to the astronomical profits on offer in the sector. Underlying fundamentals of the balance sheet of the company were ignored, and to make matters worse, Evergrande has pre-sold around $200 billion worth of incomplete projects. Missed interest payments on bonds punctuate the financial press, further defaults loom, and shares in the company are down 85% for the year. The CCP seems unwilling to bail out the company, and its price of funding is sky-rocketing. Contagion is setting in, smaller companies are also defaulting, and the wider economy is now at risk. The fear is that as each company faces up to owing much more than the value of its half-built assets, and as the market begins to take a closer look, funding will dry up, leaving more incomplete homes, more suppliers out of work, more unemployment, and social unrest. Property owners across China have staked all their hopes and dreams on the riches real estate appeared to offer, and are facing a steep drop off the wealth cliff. There are eerie parallels to the collapse of the American subprime mortgage crisis in 2007, which eventually led to the wider crash of the Global Financial Crisis. In banking and finance terms, a liquidity crisis is looming, and one which many are seeking desperately to avoid.

Normally these crises are caused simply by the inability of global finance to regulate itself. As easy credit flows, banks throw caution to the wind, lending grows so large and unsustainable that a minor shock or surprise throws the whole system off balance, and a systemic collapse is merely a heartbeat away. However, in this instance, Xi has purposely called time on the bubble. Concerned with the rampant bubble, where apartments sell at 20x income multiples, millions of homes lay empty, and the teetering developers risking overall financial stability, in 2017 Xi stated the radical notion that “housing should be for living in, not for speculation”. These words were followed up with a government policy to curtail speculative lending known as the “Three Red Lines”, where if developers exceeded three measures of risk on their balance sheets, they would no longer be able to access local funding. Evergrande is the first major developer to hit the three red lines, causing the current spiral. To reiterate, Xi and the CCP have chosen to institute a regulatory policy that they knew would cripple their domestic realty industry, and the longer they decline to offer a bailout of the developer, the more likely this contagion will spread to the global markets and economy.

This is tantamount to declaring war on global finance. To suggest housing should be for accomodation and not speculation is in itself is a truly revolutionary statement in the West (imagine the Australian Labor Party running that angle), but to follow up with policy actions was deemed a bluff by global markets. It’s only in the past month that investors, media and policy makers in the West have started to promote the Evergrande story as further evidence of Xi’s unflinching attack on capitalism. The Economist lead with “Xi Jinping is waging a campaign to purge China of capitalist excesses”. As the collapse slowly progresses, and contagion spreads, the markets are playing cool towards the prospect of a wider systemic issue. But the risk remains, and so too does global exposure to the Chinese real estate market. Currently bonds on Evergrande debt are trading at 20 cents to the dollar, a sure sign that everybody knows they won’t be getting any money back, but still investors and analysts in the media expect a Chinese government intervention. So far though, the CCP haven’t indicated any intention to provide a mass bailout a la Washington to Wall St in 2008, and look prepared to let a wider collapse of the bubble to continue.

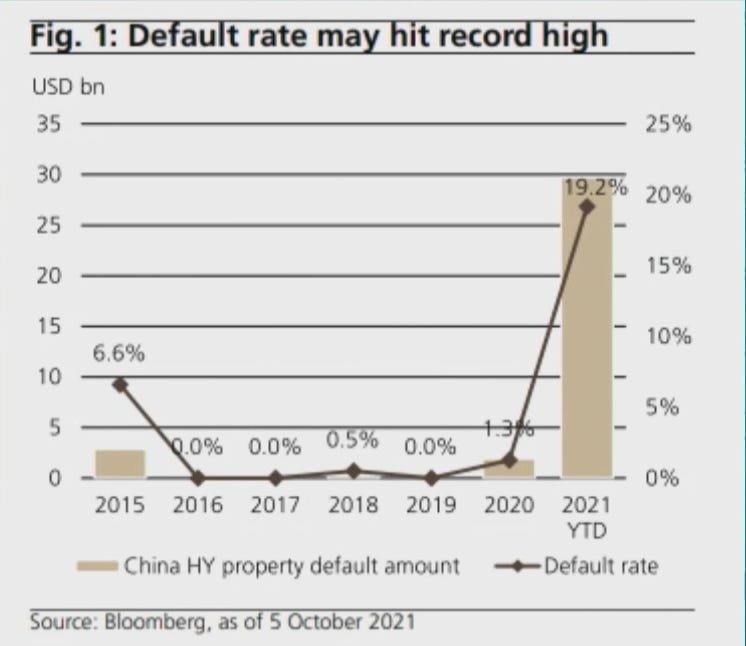

And now for the point of this newsletter: it does appear Xi is purposely engaging in a controlled demolition of the debt bubbles that pervade the Chinese economy. In turn, as defaults and contagion spread, he will be accused by the global markets of targeted destruction of the junk bond markets which are exposed to the realty bubble. The simple fact is that this type of mass default is going to cause a tide of write-offs in the West, and Xi knows this. Check this graph:

Global capitalism is at an absolute crossroads, debt levels are the highest they’ve ever been, interest rates the lowest, and inflation is rolling through all markets at an increasing pace. The pain felt by a contagion would be immense, at a time when the slack in the system and underlying growth has been hammered by the Pandemic. So why is Xi undertaking such a risky gamble, no doubt risking local stability and wealth, in order to pop the bubble?

Here is a graph that indicates why, showing the compounding monopoly-man effect of a finance bubble in a debt-fuelled market. This type of bubble has resulted in an estimated 65 million homes sitting empty.

As stated earlier, Xi identified in 2017 that this excessive speculation was an issue. It does make one wonder, how does a nominally ‘Communist’ economic system produce outcomes such as this, where a real estate developer ran by a billionaire can have a hand in the largest finance-driven realty bubble in history? The answer is that the Communist label has long expired its utility; the Chinese state throughout the 2000s and 2010s embraced market reform and multinational corporations as drivers of growth, helping China ascend to the top as the largest economy on Earth. Now, having fully utilised the rivers of credit that global capital provides, Xi has decided to call time on the party; when this bubble pops, the state will begin to nationalise the land developers, the construction companies, and even actual apartment complexes. These assets, worth a fraction of what they were 12 months ago, will then be redistributed across the populace, in a massive re-assertion of the command economy. This is 21st century socialism in action, and all we can do is watch and hope that finance speculators in the West aren’t in over their heads either. The chances of that, well, on past indicators, are pretty low.

I have veered sharply from history, to analysis, through prediction. Take it with a grain of salt, as uncertainty rules the day. But on all appearances, Xi is banking on being able to control the deflation of his bubble; in doing so, it may cause the larger global bubble to rapidly and uncontrollably explode. Policy makers and Reserve Banks have little to no room to move in response, except for further rounds of Quantitative Easing and helicopter cash. A massive risk is emerging, and the financial system is more vulnerable than anyone can understand. The anger and accusations of wilful destruction will be unending, and seen as the first real blow in the impending Chinese - US conflict.

I will leave you with a quote though, from 1978, from a US Reserve banking official: “A controlled disintegration in the world economy is a legitimate objective for the 1980s”. This man, Paul Volcker, became Chair of the Federal Reserve in the 1979. He did indeed pursue the controlled demolition of global finance markets, in order to curb rapid inflation. Whilst the United States came out far stronger from the rate increases, many smaller countries were wiped out trying to pay back US dollar loans. The US didn’t and doesn’t care about the international consequences of its decisions, it makes them in their own interest. To think the Chinese are a particularly dastardly bunch is a bit silly, naive, and ahistorical.

The Chinese Communist Party is not undertaking any particularly new or novel strategies in its ascendance, we just haven’t seen a challenger of this size take on global finance in our lifetimes. As the Chinese State reasserts itself on its markets, be prepared for the American State to respond in kind. The two poles of American power, the US Federal Government and Wall St, already almost fully entwined, will network further with the Military Industrial Complex, and a Fascist state will exist in structure, if not in status. What we will have is a near total recapitulation of the Cold War: rather than the Red Russians, it’s the Red Chinese facing up to a damaged and frightened America. History rhymes, it rarely repeats.