House of Cards

Real estate is a debt-fuelled Ponzi we can't afford to acknowledge

Ancient Chinese philosopher Lord Shang, writing 2500 years ago, observed that the pursuit of profit is entirely predictable, “just like the tendency of water to flow downhill”. I, for one, don’t argue with Lord Shang’s observation. But what if the amount of water flowing is such that it is likely to cause a flood of immense proportion? Although the ancient kingdoms of China had intricate coinage and debt recording systems, modern economies have taken on characteristics far beyond traditional modes of understanding. Human motivations remain the same, but the systems of money and debt we live by have changed immensely in the recent past.

The previous two newsletters were an attempt to background the major forces driving modern economies. These forces are government deficit spending, the lowering of interest rates to stimulate debt-fuelled expansion, and finally emergency ‘quantitative easing’, where central banks conjure cash from thin-air to further increase liquidity in the system. All these policies rely on the creation of debt, pulling future money into the present, on the belief that repayment will occur, with interest paid in the meantime. Our central bank, the Reserve Bank of Australia, controls the money supply and cash rate, i.e. the amount of debt banks and financiers can access to lend out, and at what cost.

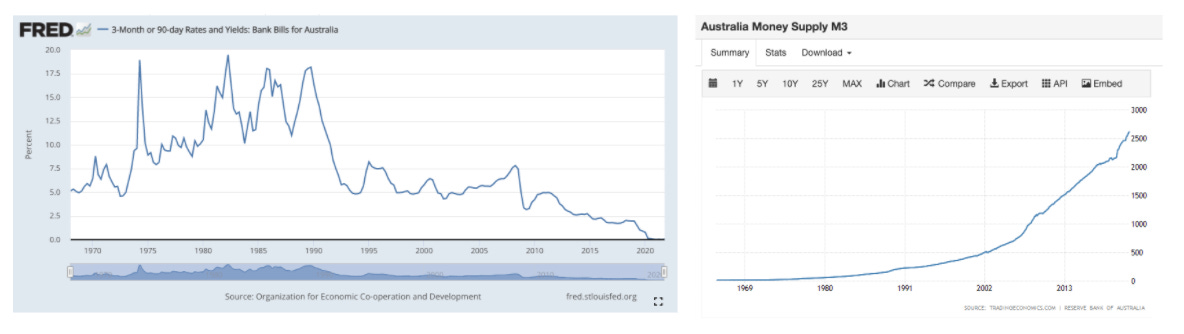

Here are the graphic representations of Reserve Bank of Australia (RBA) activity over the past 50 years, with the cash rate on the left, and overall money supply on the right.

As we can see, interest rates have been nosediving for 30 years, whilst the overall money supply is shooting for the moon. The RBA has been cutting interest rates in order to stimulate the economy, the idea being that with less cash being directed towards interest payments on mortgages, Australians will spend more in the economy. As rates have trended downwards over the past 2 decades, the RBA has simultaneously been engaging in increasing the overall money supply to also stimulate commercial and business lending. Again, these policies are undertaken in order to stimulate real economic investment and activity. These are the major policy tools of a central bank in order to attain full employment in the economy, whilst balancing inflation.

All this cheap cash, which has become essentially free if you’re a bank, has to land somewhere, and with a tax system that classifies residential housing as a legitimate investment vehicle, it has been funnelled into real estate, rather than business investment. Whether it be detached homes, townhouse development, or apartment buildings, housing is the major driver of household wealth in Australia. And whilst the going has been good for a fair while, strong economic headwinds threaten to topple the housing house of cards.

A Ponzi scheme is defined as a “form of fraud that lures investors and pays profits to earlier investors with funds from more recent investors. The scheme leads victims to believe that profits are coming from legitimate business activity, and they remain unaware that other investors are the source of funds” (emphasis added, thanks Google).

Look closely below at the correlation between housing finance growth and property prices. The rise in prices is almost totally reliant on the rise in debt, and vice versa. Two thirds of that new debt is undertaken first home buyers entering the system, whilst another third is by investors. This isn’t a natural market where prices respond to supply and demand; there is a debt pile getting larger and larger over time, feeding into higher prices. I do wonder whether most property owners understand the true source of their wealth:

Yes, overall net wealth is growing, but that is a function of more debt. As explained in previous newsletters, this is not growth in the traditional sense (“legitimate business activity” as defined earlier), rather the result of a historical process of easy access to credit that has decoupled asset values from underlying market fundamentals. Housing is a massive bubble that no-one wants to burst, and ensuring first home buyers take on large debt is the key. Whilst national home-ownership rates have been steadily decreasing since the mid 1990s, prices themselves continue their upward march uninhibited due to the flood of overseas investor money. Average mortgages are three times larger than when I was born in 1990.

One argument often presented by the older generation is that rates were way higher back in the 80s and 90s. Unfortunately this doesn’t stand up to scrutiny. In nearly all capital cities, average monthly mortgage costs are as high as they were at the peak of rates under Keating in the early 90s. The long-term overall trend is upwards, saddling families with higher cost of living to maintain rising property prices:

John Howard was a man who understood the political benefit of rising house prices. Queried about the market in 2003, Howard explained that the global “sustained period of very low interest rates” has led to a higher price structure around Australia: “I don't get people stopping me in the street and saying, 'John you're outrageous, under your government the value of my house has increased'”. Indeed, for everyday Australians, the vast majority who are not renting, it appears to be just one of those features of modern Australia, whether it’s a Ponzi or not. Nothing is safer than bricks and mortar.

Even back in 2003, there was an understanding that first home buyers were the ones being shafted with ever higher mortgage commitments, but Mr Howard was clear that "there is a problem if you're trying to get in and I can't promise that we're going to be able to slash the cost, I can't do that”. Very well. Howard launched an inquiry into ‘housing affordability and supply’, but no major policy settings were adjusted. Multiple grants have been established to help first home buyers, but none tackle the main driver of house prices: interest rates. The RBAs own modelling from March 2019 indicates clearly that cash rate changes are the main cause of price movements in the market. Multiple federal and state inquiries have analysed and reported on this issue since 2003, but no government, state or federal, seems capable of tackling the RBA and the banks head on. Treasurer Josh Frydenberg announced another inquiry last year, as the situation continues to worsen significantly. Here is the average mortgage payment increase over the past decade, compared to average full time earnings:

Now again, most Australians have processed these complex dynamics into one mode of action: buy property, and as much as you can possibly afford, because being on the ladder is better than being off the ladder. Of course, this has been true, up to now. Those who have joined the home ownership brigade earliest have benefited immensely from the rises in property prices. However, most crucially, this household wealth is fully dependent on new debt commitments by first home buyers and investors. For first home buyers to be able to enter the market, some sense of price sanity needs to be maintained, and economic conditions (jobs, spending, trade) also must be conducive to taking on a lifetime of debt. There’s also the negative effect of house prices on spending in the economy (actual spending creates jobs, not asset values). The RBAs own modelling states very clearly that high levels of owner-occupier mortgage debt reduces household spending, meaning we are boxing ourselves into a corner. Over the past decade, buyers have had to engage in ever more debt to enter the market. And far from a crash occurring due to the Pandemic, the ‘emergency’ monetary policy measures of the RBA such as quantitative easing (discussed last newsletter) have shot prices to the moon.

Crucially, this decade long boom has crowded out all other forms of investment in the economy. With these kinds of returns on offer, Australians see property as the wisest, safest, best performing possible investment. It is no wonder that a whole industry of property gurus has blossomed, hawking the secrets of the tax system and credit access, offering the dream of financial security through a personal fiefdom of negatively-geared cookie cutter rental townhomes.

One of the deepest misunderstandings of modern political and economic thought is that there is a ‘growth at all costs’ mindset present in policy makers. The real estate bubble, amongst others, indicates this to be false. If government and business were interested solely in growth, tax policy would look very different. There would be redistributive tax policies which deliver for lower income workers, who are certain to spend the extra money in their pockets, stimulating the economy. Real estate, a non-producing asset, would be taxed higher than business and corporate rates. This is crucial: whilst ‘negative gearing’ remains in the policy settings, it unfortunately makes perfect sense for a middle-class family to invest in property, ahead of shares or starting their own business. Owning a rental property does nearly nothing to stimulate the wider economy, with the only return being delivered to the banks in the form of interest payments. And although Bunnings proves we love to consume and spend on our homes and renovations, that money would be much better allocated as capital in growing businesses and employment, or buying tools and machinery. Every dollar sunk into an outer-suburbs volume build home or inner-city apartment is a wasted opportunity to invest in our productive capacity. Australian laws and policies aren’t growth at all costs, rather they are the product of donations from special interests, in this case banks, developers and the realty industry, and fossil fuels and mining in the wider economy.

For perspective, it is believed around 5% of the homes (70,000) in Melbourne are currently empty, and sit empty year on year. This is only possible due to the tax and incentive structure which means there is more return on offer through pure speculation than a rental return. This is supreme proof that a typical ‘supply and demand’ market does not exist in residential property. Rather, we have a speculative bubble fed by more and more debt. The other function of this bubble is the ability of those whose house has increased in value to access these funds in the form of ‘equity’. Say a family’s house has increased in market value from $800,000 to a million, and they would like to access some of that for renovations. They can do this through accessing their ‘equity’, increasing their mortgage to the bank in exchange for the cash. Equity loans enable home owners to use their wealth as an ATM. Now, as explained earlier, that equity is purely a function of new debt taken by first home buyers or investors. This access to recycled credit has become a central pillar of the Australian economy. True data is hard to find, but independent economists have estimated Australians take out somewhere in the range of $100 billion yearly in equity loans. Combined with government deficit spending, something like $200 billion in Australian consumption is funded by new debts, which translates to most of the growth in our economy. That growth, funded by debt, requires interest payments. What happens when interest rates change?

As previous newsletters discussed, globally we are approaching an inflationary moment of acute danger. If central banks worldwide choose to raise interest rates, which they look likely to do, the RBA will likely be forced to follow. I don’t necessarily agree that this is the only and best course of action, but I am a nobody. Look back to the 70s and 80s, central banks raised rates to counter inflation (my newsletter on Evergrande touched on this). Banks will in turn pass the rate rises onto mortgage holders to maintain their margins. The real economy is struggling under the weight of the Pandemic, and adding higher mortgage payments will depress spending and confidence even further. This will lead to an overall contraction in the system, and a decline in house values. Whilst a controlled drop in housing prices is seemingly good news, the danger of millions of homeowners owning a mortgage worth more than their property remains, the dire situation in the US that preceded the GFC. We are in un-chartered waters, and the RBA has very few policy options left.

Just for a second, let’s consider a case-study comparing the effect of the GFC on house prices in the US and Australia. The US and Australia experienced wildly divergent consequences of the GFC due to a variety of factors. Critically, Australian asset values (as explained in previous newsletters) held firm and then grew rapidly as the income from iron exports flooded in from China. Without the decision of the CCP to engage in the largest debt-fuelled economic and construction stimulus since Roosevelt’s New Deal in the 1930s, Australians too would’ve suffered a similar desperate fate to our American friends. Whilst capital city prices in Australia on average increased over 5% for the decade from 2006-2016, the average American was still behind where they were in 2006. Due to the miracle of compound interest, an average Sydney home nearly doubled over the decade to be worth a million Australian dollars by 2016. In the US, home values went backwards over the decade. It doesn’t take much imagination to wonder how in that environment and context a politician such as Trump can be a vessel for people’s anger. We best look very closely at the economic factors that lead to these ‘unexpected’ political ramifications.

So, we have a housing ‘market’ separated from supply and demand, juiced by government incentive and deficit, enabled by easy monetary conditions and the creation of free money by the central bank. Deep down we all know it cannot continue indefinitely, but instead of discussing the true causes or tackling the issue, we rejoice.

Real estate agents are easy to hate, but unfortunately, they reflect a much wider rot in our society, best exemplified by the loss of Labor in 2019. I don’t like Shorten at all, but the policy agenda put forward by Labor was fair and balanced, with the repeal of negative gearing one of many policies that would help reduce domestic housing investment incentive, allowing the lower middle classes to gain a foothold on the property ladder. Labor very nearly won, but the banks, property developers, listing websites and real estate agents were more than happy to proclaim the election a referendum on property investment and tax breaks, with the winner being house prices and the Australian realty obsession.

But the simplified binary of ‘renters vs owners’ is also false. It doesn’t adequately describe the situation, or account for the rivers of capital flowing into Australian property from overseas. What’s more, it distracts from the greater issue. Australian banks have benefitted immensely from the housing Ponzi, despite arguing they have been facing margin pressure due to falling rates. The banks make money either way, and as the overall mortgage commitments increase (currently standing at $2.2 trillion dollars), the prospectus of interest rate increases suit the banks quite well. Financialisation of the economy, in the form of more debt, benefits the banking and investor class the most. This class, the top end of town, has been doing quite well:

Steadily, the top 1% (red) and top 10% (green) have been increasing their share of national income to levels not seen since the end of World War Two. The top 1% in Australia earns nearly as much as the bottom 50%, which includes those on average salaries of nurses and teachers. The rise in inequality has developed in tandem with a drop in interest rates. Far from a force for equality, lower rates have acted as a force of intense social division, ending the Australian dream of owning a home for many. Successive governments, Liberal and Labor (thanks Keating) pander to the investor class, to the detriment of the wider economy and employment. As we can see above, the ‘renters vs owners’ narrative does quite the spectacular job in turning the working and lower middle class on itself, young versus old, masking who really benefits from the massive debt pile at the core of housing in Australia. Anyone who believes Australia is a classless society is either blinded by their own personal situation, or cannot comprehend rather elementary statistics. Choose your poison.

As the global economy splutters out of the Pandemic, and inflation rears its head, what will the RBA do? What will government do? One option being discussed is negative interest rates, which translates to the central bank paying banks to lend more newly minted money. What could go wrong? When the answer is always more debt, we are handing future generations a crippling burden. And just like climate change, we continue to do so because we will not wear the sacrifice and consequences in the meantime, if we are lucky.

This is why some label the RBA and the major banks the ‘Australian Banking Cartel’. It is also why a political candidate such as Dylan Alcott is a huge problem. We need less leaders on the payroll of major corporations, not more. When Alcott asks us to ‘draw down our debts’, one wonders whether he has any knowledge of the financial outlook for most Australians, or has experienced any of the downsides of the mass financialisation of the economy that has occurred over the past 30 years. An Australian champion on the court, for sure. A champion for all Australians? Not whilst on the payroll of ANZ.

We are a nation that willingly chooses to ignore issues. We can’t talk about the past, lest we upset our current fragile balance (hey January 26). This apathy has led us to be consoled by a realisation that we cannot do anything about the present either. It is pathetic. We embrace and joke about our reality as a coping mechanism, but we collectively have led ourselves into a gilded cage. When the conditions change, and we are no longer the lucky country, who will we have to blame but ourselves?