Collapsible Boat B

We're known as the Lucky Country after all. Best not to squander it

After last week’s rather apocalyptic diagnosis of the state of the world, I thought I’d share some reflections on a few things, current events both at home and abroad. Icebergs ahead!

Collapsible Boat B was one of the lifeboats on the ‘unsinkable’ Titanic. You had to be extremely lucky to make it on to Collapsible Boat B, even luckier to make it through the night and to safety aboard the Carpathia. Australia is a resource rich island, blessed with ample space and natural wealth. We are also our own lifeboat in troubled times, currently shackled through economic, military and political ties to the United States. How will the US combat the rising Chinese/Russian power bloc? Will Europe hold in solidarity through the winter? Will we go down with the ship? These were the questions I attempted to address last newsletter, and this article builds on those discussions with a focus on how we fit into the bigger picture, informed by my current time in Indonesia.

Many if not most of the Atlantic elite thought the Titanic was unsinkable, as many of their descendants believe the United States led world system is today. And for good reason. I made the case last week that the US dollar, the engine of global capital, may be entering a period of eventual (or sudden) decline. Whilst all those possibilities are plausible, nothing is certain. In the meantime, decisions and events cascade, causing all manner of intended and unintended consequences across the globe. The clearest display of this has been the rising US dollar in recent times:

This is the “Dixie”, a measure of the US dollar against a basket of Western currencies. As we can see, all year the dollar has been gaining significant strength. The reasons for this are many, but simply, as the Fed raises rates, foreign traders and currency dealers look to the US for those higher rates. Traders the world all over instinctively flee to the US when things get tough, or look shaky.

This graph represents the trade weighted US Dollar index against Emerging Markets. As we can see, when the pandemic eventually reached Wall St consciousness in early 2020, a mass global sell-off occurred. Everybody wanted hard dollars. It’s not as if things were great in the US, in fact as we all know things were pretty shit, as they were everywhere else. But the US has the unique ‘superpower’ to attract monetary support to itself in times of crisis, even when it may be the country causing the issues. This is known by the Europeans as the “exorbitant privilege”. One of the main drivers of the creation of the Euro was France and Germany seeking to free themselves from the spell of the dollar. The US drives economic policy the world over, for its own ends. It also means if you are a smaller nation, economically, you are at the mercy of the dollar.

In financial markets, it’s called ‘The US dollar wrecking ball’. And not for nothing. This phenomena ruined Latin America in the 80s. Ironically, it destroyed those countries most aligned with the US and global debt system far more than those isolated to the dollar. And history looks to be repeating.

The dollar wrecking ball came to being when the US decided it needed a new way to finance the Vietnam War, which was bankrupting the country. Collectively, there was a growing realisation amongst other nations that the US didn’t have enough gold to cover its debt obligations on global markets. It’s complicated to explain, but at the end of World War Two, a global system was designed to manage capital flows. This system came to be known as Bretton Woods, and underpinned global commerce for 30 years. Central to the idea was fixed exchange rates between currencies and nations, helping financial markets to avoid the booms and busts which characterised the globe in the lead up to the great wars. Implicit in Bretton Woods is the idea that by fixing exchange rates, no single country could unilaterally break off and print massive deficits for spending, with the further hope it would prevent mass militarisation and a repeat of the previous 50 years of global conflict and destruction.

But in a moment of crisis, this global agreement mattered little to the Americans, who despite having overwhelming advantage in technology and force, couldn’t manage to suppress a small south-east Asian nation’s desire for self-determination. The bombers, the missiles, the patrol boats, the chinooks, the amphibious vehicles and half a million troops on the ground cost a lot of money. US gold coverage had fell from 55% to 22%. Rather than stop the war, or stop spending, both politically toxic choices back home, Nixon and his team decided that Bretton Woods would have to go. Rather than play by the rules (which ironically they had a big say in to their advantage), the dominant position of the US in the global economy and security architecture allowed their policy makers to do whatever was needed to escape the rules everyone else had to follow. There was no-one to check their power. It’s important to note they had no back-up plan for things to work, nor could they unilaterally usher in a working solution to help manage such a transition. One evening on live TV in August 1971, speaking to the American public, Nixon blew up the global financial system. Chaos on global markets ensued. The rest of the world watched on as US Treasury Secretary John Connally famously said:

“The dollar is our currency, but it’s your problem.”

As nations around the world attempted to control the swings of the dollar wrecking ball over the following years, Connally’s successor, George Schultz added:

Obviously, these massive changes in the global system, over time, resulted in new arrangements and accomodations. There was no total collapse, at least not in the West. Combined with an energy crisis, unshackling the dollar from gold set off a decade of global inflation. Poorer countries had to borrow to keep up, accumulating huge amounts of debt for essentials like energy and food. Credit card balances in the West are also growing at an unsustainable rate, as families seek the means to keep up. Inflation always hits the poorest hardest, because there is always someone wealthier who can outbid the needy, whether locally or globally.

It’s important to realise that the same power dynamics remain today. Although China and the Euro have currencies that have global weight, and they too can print themselves out of trouble to a degree, they are currently getting smashed by the dollar wrecking ball. The energy crisis discussed last week has evolved rapidly, with political deals being tabled to tackle the crisis in the UK and Europe. Most of the proposed policy options rest on huge government spending bailouts and price guarantees. Most of the countries in the “third world” do not have the luxury of such options. Unable to pay inflated global prices for petrol, food, and essentials, smaller countries run out of money. Sri Lanka’s collapse last month was the first domino to fall in many.

Here’s an excerpt from guest essay in the NYT by Indrajit Samarajiva, reporting on the situation, detailing how reality on the ground mirrors current global dynamics:

“I have a car, which has now turned into a giant paperweight. Sri Lanka literally ran out of gas, so my kids asked if they could play inside the vehicle. That’s all it is good for. Getting fuel required waiting for days in spirit-crushing queues. I gave up. I got around by bus or bicycle. Most of the economy stopped moving at all. Now fuel has been rationed, but irrationally. Rich people get enough fuel for gas-guzzling S.U.V.s while working taxis don’t get enough and owners of tractors struggle to get anything at all.”

Say a country is in massive debt at the moment. The reasons for each countries difficulties are unique in many ways, but also are the result of historical realities that we like to avoid when talking in the present tense. Many countries are still in debt for deficits from the original inflationary cycle in the 70s. They can’t print their way out the situation, because their currency will dissolve (see Turkey). However, if you remember, the US currently sits on $23.3 trillion in government debt. It also rules the world with an iron fist. See the connection yet? The dollar wrecking ball is central weapon in US economic dominance; sometimes you don’t need the military to do all the work. The military dominance underpins the currency dominance, and vice versa, printing the currency allows for spending on the military. That’s all the dollar is, an IOU from the US government that it will rule the world in perpetuity.

Europe’s energy issues are not over yet. Traders and speculators are diving into the market, and their risky bets may also require a massive bailout now, reminiscent of the bets on housing in 07/08. When an economic and political system embraces a casino mentality for basics like food, water, housing, these are the consequences. Western societies are in economic danger this winter. But what results in recession and unemployment in the West is bread riots, starvation, protests and social unrest in the poorest parts of the world. Back to Sri Lanka, Mr. Samarajiva reports:

“Many Sri Lankans are going on one meal a day; some are starving. Every week brings to my door a new class of people reduced to begging to survive.”

Just like in the 70s and 80s, these struggling nations will seek assistance from more powerful countries. Assistance comes in many forms, but mostly comes in the form of credit to pay for the necessities. The International Monetary Fund (IMF) is known as the lender of last resort. It offers lending to struggling countries in desperate need, but with conditions attached. These conditions include privatising and selling off infrastructure to Western investors, or gutting social spending on health and service budgets in order to ‘tighten belts’, a euphemism devoid of all reality when one takes a second to consider global obesity and consumption rates.

There’s this great book from 2004 by an American development consultant called Confessions of an Economic Hitman. From wikipedia:

“According to Perkins, his his job at the firm was to convince leaders of underdeveloped countries to accept substantial development loans for large construction and engineering projects. Ensuring that these projects were contracted to U.S. companies, such loans provided political influence for the US and access to natural resources for American companies, thus primarily helping local elites and wealthy families, rather than the poor. According to Perkins, he began writing Confessions of an Economic Hit Man in the 1980s, but claims "threats or bribes always convinced [him] to stop."

Confessions of an Economic Hit Man, with the byline “the shocking inside story of how America REALLY took over the world”, was written in 2004. Skip forward 18 years to Sri Lanka and Mr. Samarajiva lays out what this looks like for the populations of countries impacted:

Sri Lanka — like so many other countries struggling for solvency — remains a colony with administration outsourced to the International Monetary Fund. We still export cheap labor and resources and import expensive finished goods — the basic colonial model. The country is still divided and conquered by local elites, while real economic control is held abroad. The I.M.F. has extended loans to Sri Lanka 16 times, always with stringent conditions. It just keeps restructuring us for further exploitation by creditors.

And as much as the West blames Chinese predatory lending, only 10 to 20 percent of Sri Lanka’s foreign debt is owed to China. The majority is owed to U.S. and European financial institutions or Western allies like Japan. We died in a largely Western debt trap.

Other countries face the same peril. Around 60 percent of low-income nations and 30 percent of middle-income ones are in debt distress or at high risk of it. Pakistan, Bangladesh, Tunisia, Ghana, South Africa, Brazil, Argentina, Sudan — the list of those in trouble is growing rapidly. An estimated 60 percent of the world’s work force has lower real incomes than before the pandemic, and the rich countries offer little to no help.

The dollar wrecking ball has become God in world affairs. It is the provider and destroyer of destiny. It demolishes smaller economies, yet is also the safe haven for the big money in troubled times. The global community preferences the flow of capital ahead of the needs of the worlds people. The US, the nation most responsible for the global inflation outbreak, is also most insulated from the effects of its policies. The cynical and conspiratorial among us wonder whether there’s a more sinister connection there: the powerful are always insulated from inflation and economic turmoil. This is mostly true within societies as it is externally between nations. The US dollar wrecking ball serves to protect US interests.

In January I wrote that central bankers had lost control of the money supply. Many wonder whether it is shocking incompetence or cunning malice that drives US economic, financial and foreign policy. The truth is probably somewhere in between. China and Russia believe pretty clearly its the latter, and are acting fast to set up an alternative to the US dollar wrecking ball. Many in the West cannot stand to hear Putin, but I would suggest paying attention to what he has to say on these issues, and not because I agree with everything he says. It is absolutely critical to listen to those we disagree with, even if we seek and desire their eventual demise.

Many of the developing nations of the world, tired of the US dollar wrecking ball, of crippling Western debt, IMF bailouts and debt traps, are listening to Putin and Xi’s proposals for an alternative. In geopolitical terms, the new Eastern bloc combined with Brazil, Saudi Arabia and India could offer a substantial alternative to the dollar in the coming years. These poor nations seek a new lifeboat in troubled times, and it’s hard to blame them.

It’s always troubling when the term “third-world country” is thrown around in Australia, and I don’t want to be nit-picky about the etymology or connotations of the word. I mean in the way people use it, to describe something as being backward and shit, not up to the standards we expect. There reasons for this happening are many, but we are not a “third-world” or “second-world” country. We can do so much better, given our relative position in the grand scheme of things. Parts of the periphery of the cities, the horrendous conditions and prospects in the outback and rural ghost towns are confronting, but the key is that we have the ability and the wealth to fix this. We can provide for free childcare, for more public transport, for a cleaner energy grid, for higher education to not be an endless credential sticker factory but rather a vehicle for opportunity and true social mobility. We have the ability to do many, many things: options that many nations and people can only dream about.

Last week I outlined how Germany’s high-tech business model relies on cheap Russian gas to subsidise the higher research, development and labour costs needed to make a quality Bosch, BMW, Mercedes whatever. It doesn’t take much of a leap to see we can do that in Australia, if we wanted to. Plus we wouldn’t be at the mercy of Putin’s pipelines. We have plentiful energy, plentiful minerals, plentiful space, plentiful brainpower, a solid rule of law. If the government was serious about a green transition, it could marshal its resources and unique ability to provide finance, and propose a new industrial policy for the times. Australia could become a renewables research, development and manufacturing powerhouse. We could eat into that 75% market share that China has on renewable tech. But don’t hold your breath. That is way beyond the scope or imagination of a thoroughly conservative Labor Party. Three months in and no meaningful rise in unemployment payments; keeping the upcoming Stage 3 tax cuts for the wealthy in a time of extreme inflation; completely avoiding the COVID bogeyman: if you want Liberal policies, vote Labor. At least the extreme corruption borne of multiple terms in power hasn’t had a chance to stick just yet. Where’s the ICAC by the way? So quickly we forget the promises made to us.

The clearest example of successive policy failures in energy and industrial policy in recent times has been the energy market failure this winter. The main cause is Australian companies sending LNG to China on an agreed price contract, way below market price, a deal agreed by Howard in the early 00s when everyone wanted to still be friends with the rising Asian power. The energy crisis in Europe and extreme price rises means that a Sydneysider is paying higher prices for Australian LNG than those in Shanghai. The tit-for-tat EU/Russian gas war has resulted in zero flows of LNG from Russia to Europe. the EU has been panic buying at extreme prices in anticipation of running out of heat in the winter. China is now on-selling discounted Australian LNG to Europe at the premium rate. You cannot make this stuff up. We can’t break our contract with China, and I wouldn’t recommend doing that either. I don’t offer any real solutions, it doesn’t matter, but I am enjoying documenting the absurdity of the current moment. If it wasn’t such a disaster it would be funny.

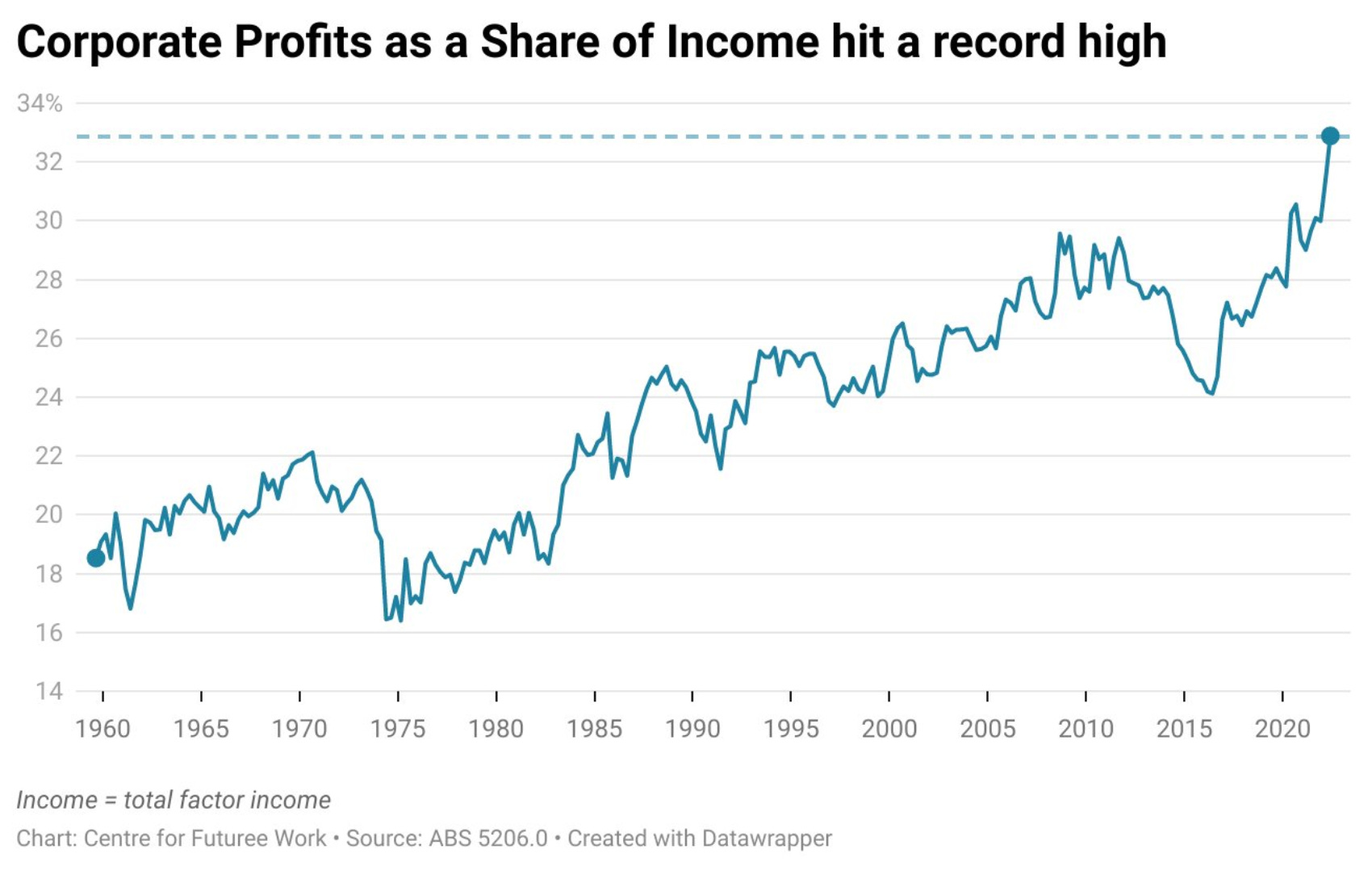

The second national policy failure is Qantas, headed by swindler in Chief Alan Joyce. The fact the man is celebrated as a smart businessman, rather than an ogre of selfishness, is a disgrace, and all you need to know to understand modern Australia. The man, his policies, are representative of a wider malaise in society. A brave government could have nationalised Qantas during the pandemic for almost nothing, then sold it back onto the market once things had recovered, making a tidy profit for the taxpayer, rather than the $2 billion+ cash handout that the Liberals decided was best. Loyal workers sacked for labour hire, service standards ruined, a rotting work culture and flights cancelled on the tarmac. Elderly passengers stranded on the boiling asphalt, outside, under no cover, with no water or snacks, for 4 hours, in Denpasar. This is Joyce’s legacy, and it’s not the fault of the pandemic. To expect anything better in Australia in 2022 might seem decadent, but the man has taken in $104 million in a decades long corporate con job. Corporate Australia is taking a rapidly rising share of the income in Australia, and has been for some time. Australia was a lot more equal back in the 60s and 70s, and it doesn’t take a genius to understand that if most of the wealth generated in the society floats upwards, people get left behind.

Greg Jericho @GrogsGamut on Twitter

Interest rates in Australia will rise in line with the decisions made by the US Fed. This is the consequence of being a moderately size developed economy in the modern globalised financial system, lest we also want to be at the mercy of the dollar wrecking ball. Being enmeshed in the global system, to the degree we are, severely limits our ability to be independent. Of course, when times are good, we applaud our integration with the global economy. The luck of having iron ore to sell to China prevented the GFC reaching our shores. It’s an unfortunate reality that all these energy shortages, and associated rising prices, actually help Australia’s terms of trade and budgetary position. I would be surprised if Labor offer anything substantive to tackle the big issues, let alone develop proposals to help with the myriad social, development and environmental issues plaguing the nation within the current framework. The argument from government and big business is that nothing can be done. Rising interest rates and inflation require that we too must ‘tighten our belts’, which is true to a degree. So why a massive tax cut for the rich? Makes you wonder?

I will probably go into detail about specifics about inflation and Australian politics and markets next time. But if we are to be a lifeboat in troubled times, we also need to try to free ourselves from the madness and swings of the US dollar wrecking ball. This requires imagination. Mixing metaphors always ends badly.